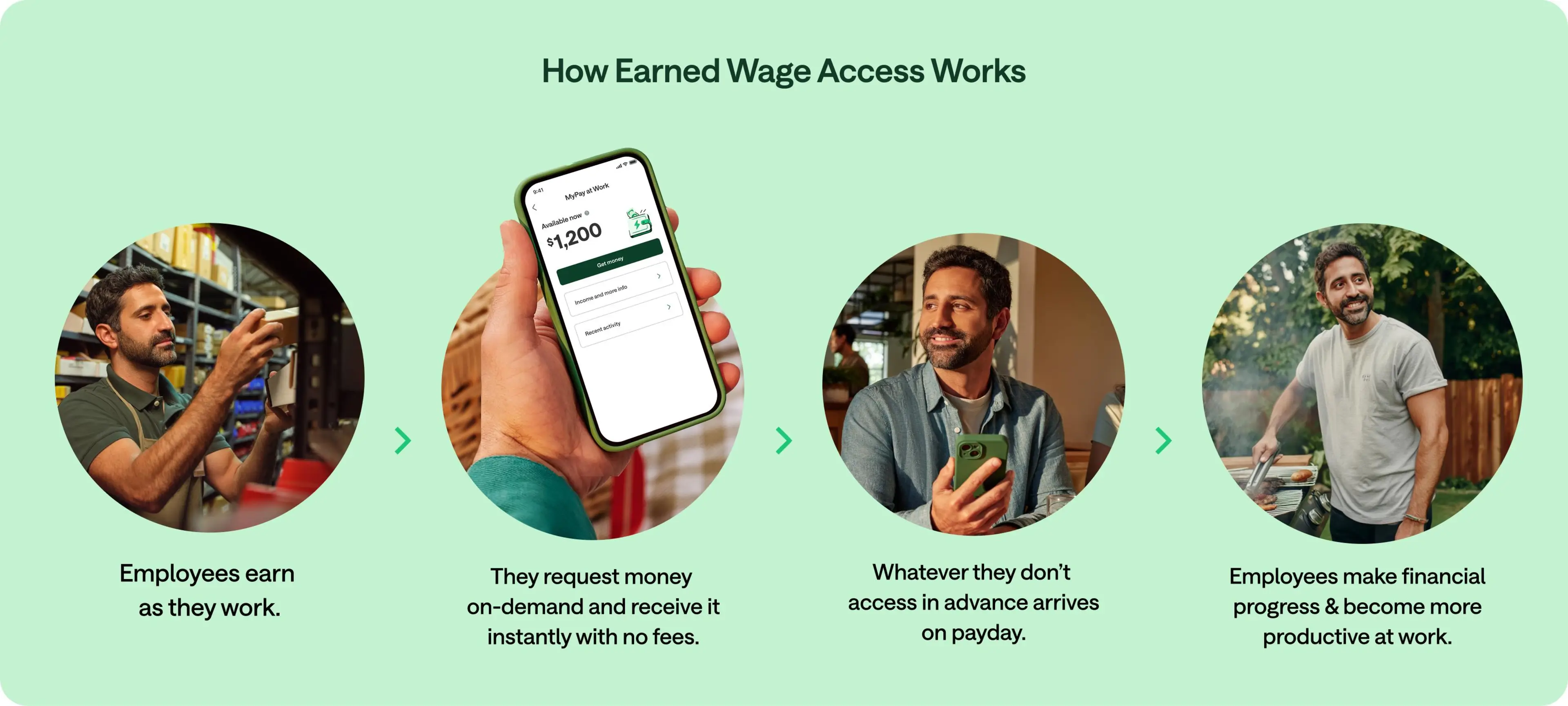

Earned wage access:

The first step to financial well-being

Give employees access to earned wages while reducing turnover and improving retention.

What is modern Earned Wage Access (EWA)?

Legacy EWA solved for access — a short-term bridge between paychecks. But as living costs rise and schedules fluctuate, access alone hasn’t been enough to keep workers afloat. Most employees are still navigating daily financial stress that follows them into the workplace—and employers feel it in productivity, engagement, and retention.

Key attributes of modern earned wage access

The first step toward stability

Provides immediate financial relief to help employees bridge short-term cash flow gaps.

Free access for every employee

Employees keep every dollar they earn with no fees to advance money. No surprises. No added costs.

Designed for modern compliance

Built to align with nationwide and state regulations.

A platform for lasting progress

Integrated with savings, credit tools, and guidance to strengthen long-term stability.

Everest Group’s State of EWA Report Marks a Turning Point for EWA

77%

77% of enterprises now cite financial wellness as the #1 driver for EWA adoption

83%

83% of employers say their financial health programs struggle to demonstrate positive financial outcomes

56%

56% of enterprises demand a no-fee EWA models

Everest Group, The Reinvention of Earned Wage Access (EWA), January 2026.

Modern earned wage access as a financial wellness gateway

Chime’s modern approach combines instant access to earned pay with the tools that help employees build long-term stability: automated savings, no-fee credit building, goal tracking, and personalized financial guidance. It gives employees a way to manage emergencies today and build better financial habits over time.

For variable-income and shift-driven workers, this becomes a critical foundation—reducing reliance on overdraft, payday loans, and high-cost credit while smoothing cash-flow gaps that often disrupt work and well-being.

Top EWA Providers Comparison

Chime | DailyPay | Payactiv | Earnin | Rain | |

EWA Fee | $0 Instant to Chime account | $3.49 Instant | $3.49 Instant (To non-Payactiv card; Walmart Cash Pickup; Visa+ Wallet); $0-$2.49 Instant (based on direct deposit to Payactiv Visa^) | $3.99-$5.99 Lightning Fee (based on transfer size); $2.99 if employee is using EarnIn Card^ | $3.99 Instant |

Early Direct Deposit | 2-day early direct deposit1 | N/A | With Payactiv Visa card^

| $2.99 per early direct deposit

| N/A |

Fee-Free Overdraft | Up to $200 of overdraft protection2 | N/A | N/A | $5.99/month “Balance Shield” tool | N/A |

Financial Wellness Offering | High-yield savings account3; credit builder; AI-enabled financial coaching; high-touch counseling^^ | No-interest savings account; credit monitoring; financial coaching ^^ | No-interest savings account; financial coaching^^ | No-interest savings account; credit monitoring | Financial coaching |

* All listed EWA vendors offer free ACH transfers to third party accounts

^ Instant transfers represent 90%+ of all EWA transactions; Some vendors offer a card option, but adoption is negligible

^^ Through partner vendor

Earned Wage Access Models Evolution

In this video:

Evolution of Earned Wage Access (EWA)

The Legacy EWA Deduction Model

The EWA Intercept Model & Regulatory Risks

Modern EWA: The Settlement Model

Why EWA Models Evolved

The Future of Earned Wage Access (EWA)

Earned wage access models (and why they matter)

Not all EWA works the same. Some models are modern and compliant, while others are outdated and risky. The underlying model determines how clean, compliant, and low-lift the experience is for employers.

1. Deduction Model

Requires employers to run payroll and deduct the accessed pay amount from the employee’s next paycheck.

Heavy payroll involvement and manual oversight

Can trigger wage-deduction and compliance risks at the state level

Creates errors when hours or shifts don’t align

Leads to “dock in pay” confusion for employees

2. Intercept Model

Providers reroute employer payroll, hold employee wages, and withdraw repayment separately.

Providers act as intermediaries in payroll

Can trigger wage-deduction and compliance risks at the state level

Higher potential for misdirected pay and errors

More ongoing resourcing & support for the program

3. Settlement Model (Chime)

Employees are paid into their own FDIC-insured account; repayment settles after payroll, outside employer systems.

No payroll rerouting or operational lift

Settlement occurs in employee-owned account

No employer funding required

Eliminates risk of misdirected payroll

What is compliance-ready earned wage access

EWA regulations vary state-to-state and minimize employer risk.

Chime’s settlement approach supports key regulatory expectations through:

Centralized provider oversight of applicable product disclosures, reporting, and product-level compliance

Non-recourse, no interest, no credit checks

Transparent, payroll-embedded integrations

Support for disclosures, reporting, and state frameworks

Earned Wage Access Laws and Regulations

Earned Wage Access (EWA) is becoming increasingly regulated to ensure transparency and consumer protection. In 2025, the Consumer Financial Protection Bureau issued an advisory opinion clarifying how certain earned wage access (EWA) is not credit under the Truth in Lending Act and Regulation Z. This federal clarity helps employers better understand the regulatory treatment of EWA, while state wage, labor, and lending laws continue to apply.

Bring financial wellness to your entire workforce.

Explore the full Chime Workplace platform with integrated EWA, savings, credit, and guidance that drive real financial progress.

Earned wage access: Payroll & HRIS integrations

Chime Workplace and EWA technology integrates directly with leading payroll and workforce management systems to deliver:

Real-time or daily wage accrual syncing

Automated deduction processing

Eligibility syncing (job role, status, location)

Secure API connections and file-based integrations

Low-lift IT setup with implementation support from Chime

Want to integrate with Chime?

See what our customers are saying about Chime Workplace

"Our goal has always been to help employees improve their financial well-being, but prior solutions limited them to just one tool. We decided to move to Chime Workplace because it offered tools including earned wage access that helped employees grow.”

Veronica Chimeny, CHRO, ETech

Previously, the EWA provider we partnered with had poor customer service. Their algorithms changed frequently, which often led to problems with advance overages and left employees with no remaining deposit on payday. Chime has offered many fee-free advance options, special perks, financial wellness options and much better customer service.

Jaime Davis, Sr Leader of Payroll, ETech

The transition from our previous earned wage access solution to Chime Workplace's comprehensive financial wellness suite was seamless and efficient, allowing us to enhance our benefits offering without disrupting operations or the high standards of care our residents and families expect.

Allie Rapini, Director of HR, Cedarhurst Senior Living

Bring modern EWA to your workforce

Modern earned wage access helps employees take their first step toward financial well-being — and helps employers build a more stable, productive workforce.

Get a demo to bring modern EWA to your team.

FAQs

What is earned wage access and how does modern EWA work?

Modern earned wage access (EWA) gives employees instant access to a portion of their earned wages before payday without changing payroll cycles or adding fees. Employees receive funds instantly into their own account, and repayment happens automatically after payroll.

What is the difference between modern earned wage access and traditional EWA?

Traditional EWA only solved immediate cash needs. Modern EWA adds financial wellness tools such as automated savings, credit building, financial guidance, and goal tracking. Employers choose modern EWA because it improves retention, stability, and productivity.

Why do earned wage access models (deduction, intercept, settlement) matter for EWA compliance?

Deduction and intercept models modify paychecks or reroute payroll, which creates wage-assignment risk and compliance exposure. The settlement model avoids payroll changes entirely and is preferred because repayment happens outside payroll.

What is the EWA settlement model and why is it the most compliant approach?

The settlement model deposits funds directly into an employee’s own account, then settles repayment after payday through standard banking processes. This avoids wage deductions, payroll rerouting, and wage-assignment restrictions across many states.

Why do employers want earned wage access repayment outside payroll?

Repayment outside payroll eliminates the need for payroll adjustments, reduces administrative errors, avoids wage-assignment issues, and minimizes workload for HR and payroll teams.

Is earned wage access free for employees, and does Chime Workplace offer true no-fee EWA?

Yes. Chime Workplace offers earned wage access with no fees, no tipping, no subscription charges, and no paid “instant” transfers. Many vendors advertise no-fee access but still charge for speed; true no-fee EWA removes all of these costs.

Does earned wage access affect payroll cycles or wage calculations?

No. Payroll cycles and wage calculations remain unchanged because modern EWA systems operate independently of payroll. Employers run payroll as usual.

Is earned wage access compliant in all U.S. states?

Modern fee-free settlement-based EWA aligns with emerging state regulations across Maryland, New Jersey, California, New York, and others. The structure avoids wage-assignment risk and fits evolving regulatory frameworks.

What does the CFPB say about earned wage access and how do new regulations affect employers?

The CFPB treats fee-based or wage-assignment EWA structures as forms of credit. Employers reduce regulatory risk by choosing fee-free EWA models that avoid tipping, interest, payroll deductions, and earned wage “advances.”

How does earned wage access reduce employee financial stress?

EWA provides immediate access to earned wages so employees can avoid overdrafts, payday loans, late fees, and cash-flow gaps. When combined with savings and credit-building tools, EWA helps create long-term financial stability.

Does earned wage access improve retention, recruiting, and shift reliability?

Yes. Financial stress is a major cause of callouts and turnover. Employers offering EWA see lower turnover, improved hiring funnels, stronger shift coverage, and better reliability.

Why is financial wellness the top reason employers adopt earned wage access?

Most employers now adopt EWA to improve employee financial wellness, not just provide early pay. Financial stability leads to better performance, higher engagement, and fewer distractions that affect productivity.

How does earned wage access integrate with payroll and HR systems like Workday, ADP, and UKG?

Modern EWA integrates through secure APIs or file connections to sync wage accruals, eligibility, job roles, and employee status. It works with systems such as Workday, UKG and others.

Why is settlement-based earned wage access lower risk than deduction or intercept models?

Settlement avoids payroll rerouting, paycheck deductions, and wage holds—practices that have been scrutinized by regulators. It reduces compliance exposure, payroll errors, and potential legal risk.

How does earned wage access improve employee productivity?

Financial stress reduces focus and reliability. When employees can cover unexpected expenses, they show up more consistently and can focus better, resulting in measurable productivity improvements.

What financial wellness tools come with Chime Workplace’s earned wage access program?

Chime Workplace includes automated savings, overdraft protection, credit building, goal tracking, financial education, and personalized financial insights. This makes EWA the entry point to a full financial wellness ecosystem.

Is earned wage access only for hourly workers, or can salaried employees use EWA too?

EWA works for both hourly and salaried employees. Eligibility depends on wage accrual syncing, not job classification. It’s widely used in industries like hospitality, healthcare, logistics, retail, and call centers.

How do earned wage access banking partnerships work, and why do some providers require debit cards?

Some EWA providers rely on debit-card-based funding models and use interchange fees to cover costs. Modern solutions allow employees to use any bank account and do not require vendor-specific debit cards.

How do earned wage access providers verify hours, wages, and eligibility?

Integration with payroll or workforce management systems allows providers to sync real-time or daily wage accruals, job role data, and employment status. This ensures accurate available-balance calculations and prevents overuse.

What is the ROI of earned wage access for employers?

EWA increases ROI through lower turnover, better retention, improved shift reliability, reduced callouts, and higher productivity. Since modern EWA requires no payroll changes or treasury work, employers gain significant value with minimal lift.