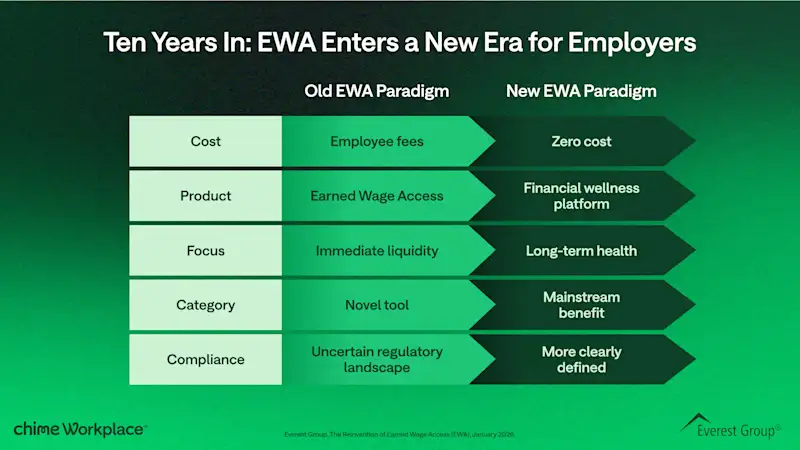

Earned wage access (EWA) has emerged as one of the more widely discussed tools in the modern employee benefits landscape — giving employees access to pay they've already earned. A decade after its introduction in 2015, EWA has expanded to millions of workers. Some market projections estimate growth up to 300% between 2024 and 2034, though forecasts vary by methodology and source.. Yet despite this momentum, a stubborn obstacle is preventing EWA from realizing its full potential: fees.

According to Everest Group's 2026 research — based on a survey of over 100+ senior payroll, finance, and HR executives — hidden and per-transaction fees are not just a minor inconvenience. Research suggests pricing structures may influence employee trust, employer risk assessment, payroll administration complexity, and overall programs outcomes.

The Promise and the Practical Considerations

The foundational premise of EWA is straightforward: employees have already earned their wages — they simply lack access to them until payday. Yet legacy EWA models built around fees of approximately $3 per instant transfer may create tension with this premise depending on frequency of use and employee circumstance. Workers who need financial flexibility most are also most likely to access wages frequently — and therefore most likely to pay the highest aggregate fees.

For employers, pricing design can influence employee perception, utilization, and internal administration. Importantly, EWA is an optional benefit. Usage patterns vary by employee, and outcomes depend on individual financial circumstances and program design.

Regulatory and Operational Considerations

EWA programs operate within a developing regulatory landscape. According to Everest Group, 62% of enterprises that do not currently offer EWA cite regulatory concerns as a key barrier.

Areas employers may evaluate include:

State-by-state regulatory requirements

Wage assignment and deduction rules

Licensing considerations

Repayment handling methods

Payroll reconciliation processes

Some models utilize “payroll intercept” structures in which the provider recoups advances at payroll. Depending on implementation, this may introduce reconciliation complexity or require additional employee communications.

Payroll professionals have indicated preferences for models that maintain paystub clarity and minimize administrative burden. In a PayrollOrg survey of 798 payroll professionals:

93% agreed EWA funds should go directly to the employee’s bank account

91% preferred that EWA programs avoid fees for both employers and employees

These findings reflect operational preferences rather than guaranteed legal conclusions. Employers should evaluate models based on their internal compliance and payroll frameworks.

Adoption Trends: What the Data Suggests

Everest Group’s research indicates that 56% of enterprises that do not currently offer EWA would reconsider if a zero-fee model were available.

Different pricing models may carry varying operational, compliance, employee experience considerations depending on how they are structured and implemented.Employee participation rates can also be influenced by:

Awareness and communication

Trust in financial tools

Perceived repayment clarity

Integration with existing payroll systems

Programs designed with transparent pricing and clear repayment structures may reduce confusion and administrative friction. However, utilization and outcomes depend on employer implementation and employee usage.

What Enterprises Are Prioritizing in EWA Evaluations

The research highlights four themes that enterprises increasingly consider when evaluating EWA solutions:

1. Transparent Pricing

Clear disclosure of any costs, eligibility requirements, and repayment mechanics.

2. Operational Alignment

Repayment structures that align with payroll processes and minimize reconciliation complexity.

3. Payroll Integration

Pre-built integrations and APIs that reduce manual intervention and support audit visibility.

4. Broader Financial Wellness Strategy

Some employers view EWA as one component of a broader financial wellness ecosystem that may include savings tools, education, and budgeting resources. Outcomes vary based on employee engagement and program design.

Considerations for HR and Payroll Leaders

For organizations evaluating EWA, pricing structure is not simply a commercial decision — it may influence compliance review, payroll operations, employee communication, and participation rates.

Fee-based models may require additional analysis regarding wage deductions, disclosures, and employee communications. Zero-fee models may reduce certain administrative considerations, depending on structure. However, employers should evaluate any model, regardless of pricing, based on their internal compliance, payroll systems, and workforce needs.

As with any employee benefit, employers should assess:

Regulatory alignment

Provider compliance posture

Payroll impact

Communication clarity

Cost transparency

EWA is an optional benefit. Its effectiveness depends on responsible program design, employee understanding, and appropriate compliance oversight.

Chime Workplace offers a comprehensive financial wellness suite designed to provide employees with access to education and fee-free financial tools that may support progress along their financial wellness journeys. To learn more about how Chime Workplace™ approaches earned wage access and payroll integration, request a demo today.