There’s a question I often hear from HR and benefits leaders:

How do we actually build a financial wellness program that works?

Over the past few years, companies have moved quickly. They’ve added earned wage access (EWA), financial coaching, savings tools, student loan assistance, budgeting apps, and more to address the varying needs of their employee population.

But there are two structural issues that have limited the impact of these benefits:

The unbanked and underbanked problem. 25 million households are still unbanked or underbanked1, constraining their ability to engage with a financial wellness benefit. Using a financial wellness benefit without a primary bank is like using a healthcare benefit without a primary doctor.

The connectivity and integration flaw. Even for the banked workers, financial wellness solutions typically don’t integrate with bank accounts, creating friction, low adoption and lack of measurable outcomes. Imagine needing a separate healthcare benefit and app for different physical ailments. So it goes with financial wellness. Employees want a single platform to manage their financial needs.

These are foundational problems, limiting the impact of financial wellness programs — especially for the employees who need them most. Fortunately, there is a solution that addresses both issues: financial wellness embedded in a no-cost workplace banking benefit.

What Is Workplace Banking

Workplace banking (workplace finance) is a model where employers partner with financial institutions to provide employees with financial benefits such as accessible, low-cost, fully integrated banking services directly through the workplace.

At its best, workplace banking is not just another account—it is a better version of banking itself, designed around how people earn, spend, and manage money through work.

It delivers four fundamental advantages:

1. Improved Affordability

When employers and financial institutions work together, they unlock lower-cost or no-fee financial services that are not typically available in the retail market.

Why? Because employer-linked banking benefits from higher fidelity data—including income, employment status, and pay cycles—which reduces risk and cost for financial institutions.

That can translate directly into:

No monthly fees

Reduced or eliminated transaction costs

Less reliance on high-cost alternatives like check cashing or payday lending

2. New Financial Capabilities Powered by Better Data

Workplace banking introduces a new layer of financial infrastructure by leveraging real-time earnings and workforce data.

This enables entirely new types of financial experiences, including:

Available earnings balances (not just checking balances)

Seamless access to earned wages

Smarter liquidity tools aligned to pay cycles

In other words, employees don’t just see what they have—they see what they’ve earned and can act on it.

3. A Connected, Seamless Financial System

Today’s financial wellness landscape is fragmented. Employees are asked to navigate multiple apps, accounts, and tools that don’t talk to each other.

Workplace banking changes that.

It creates a connected, one-stop financial ecosystem where:

Banking, saving, spending, and borrowing live in one place

Employees can move seamlessly between products

Tools adapt to where someone is in their financial journey

This isn’t a bundle of benefits. It’s an integrated system—with banking as the foundation.

4. Employer Outcomes

Workplace banking may be an employee benefit but it benefits employers too:

Higher direct deposit adoption, reducing costs associated with paper checks and pay cards

Greater workforce productivity2 as workers build emergency savings

Improved retention3 as financial security rises

Lower rates of absenteeism4 as financial stress declines

Employers can even monitor workforce financial health (on an anonymized basis) through a dashboard that tracks savings rates, credit health, and financial stress.

Why Workplace Banking Matters Now

According to FDIC data1, 5.6 million households are unbanked and 19 million are underbanked. And this issue is not evenly distributed — it disproportionately impacts hourly and frontline workers, the same populations employers are trying to support through financial wellness programs.

If someone is:

Managing cash flow through check-cashing services

Paying fees just to access their wages

Lacking emergency savings

Then most financial wellness tools simply don’t land. A budgeting app doesn’t resonate. A savings program has nowhere to live. Financial coaching becomes theoretical.

But even beyond access, there’s a second issue: disconnection. For employees who do have bank accounts, financial wellness tools are often completely separate from where financial decisions actually happen—their bank account.

It’s as if a wall has been built between:

The benefits employers provide

And the financial reality employees live in daily

They are not getting the full value of financial wellness benefits because there is a lack of integration between the benefit and the bank account. Financial coaching is divorced from everyday financial decisions. Emergency savings accounts (ESAs) can’t be accessed where workers bank. It’s as if a wall has been built, separating the benefit from the employee’s financial hub - the bank account. That’s why 91%5 of financial app users prefer a platform to meet all of their needs, rather than multiple point solutions.

As a result, employers are increasingly including no-cost workplace banking (aka employee banking) in their financial wellness programs to:

Address the problem of the unbanked/underbanked by providing fee-free access to critical banking services.

Solve the integration problem by embedding financial wellness tools in the workplace banking experience.

Why Employee Banking Is More Accessible Now

For a long time, expanding access to banking required physical infrastructure — branches, local presence, eligibility requirements. That constraint no longer exists.

Today, a mobile-first model allows employees to open and manage a full-featured account with nothing more than a smartphone and a payroll connection. Barriers like minimum balances, geographic limitations, and complex onboarding have largely been removed.

At the same time, financial wellness has moved from a “nice-to-have” to a strategic priority for employers. Financial stress is a productivity killer:

Workers spend 6.4 hours2 per week distracted by money problems

Financially stressed employees are 34%4 more likely to be absent or late

Financially insecure workers are twice3 as likely to be job searching

Employers are no longer asking if they should invest in financial wellness. They’re asking why it isn’t working as well as it should. The answer increasingly points to the same place:

The foundation is missing.

How Workplace Banking Makes an Earned Wage Access (EWA) Benefit More Impactful

Earned wage access (EWA) is one of the most important innovations in financial wellness over the past decade. It solves a real problem — the timing mismatch between when people earn wages and when they need to use them. For many employees, it reduces reliance on high-cost alternatives and provides immediate relief.

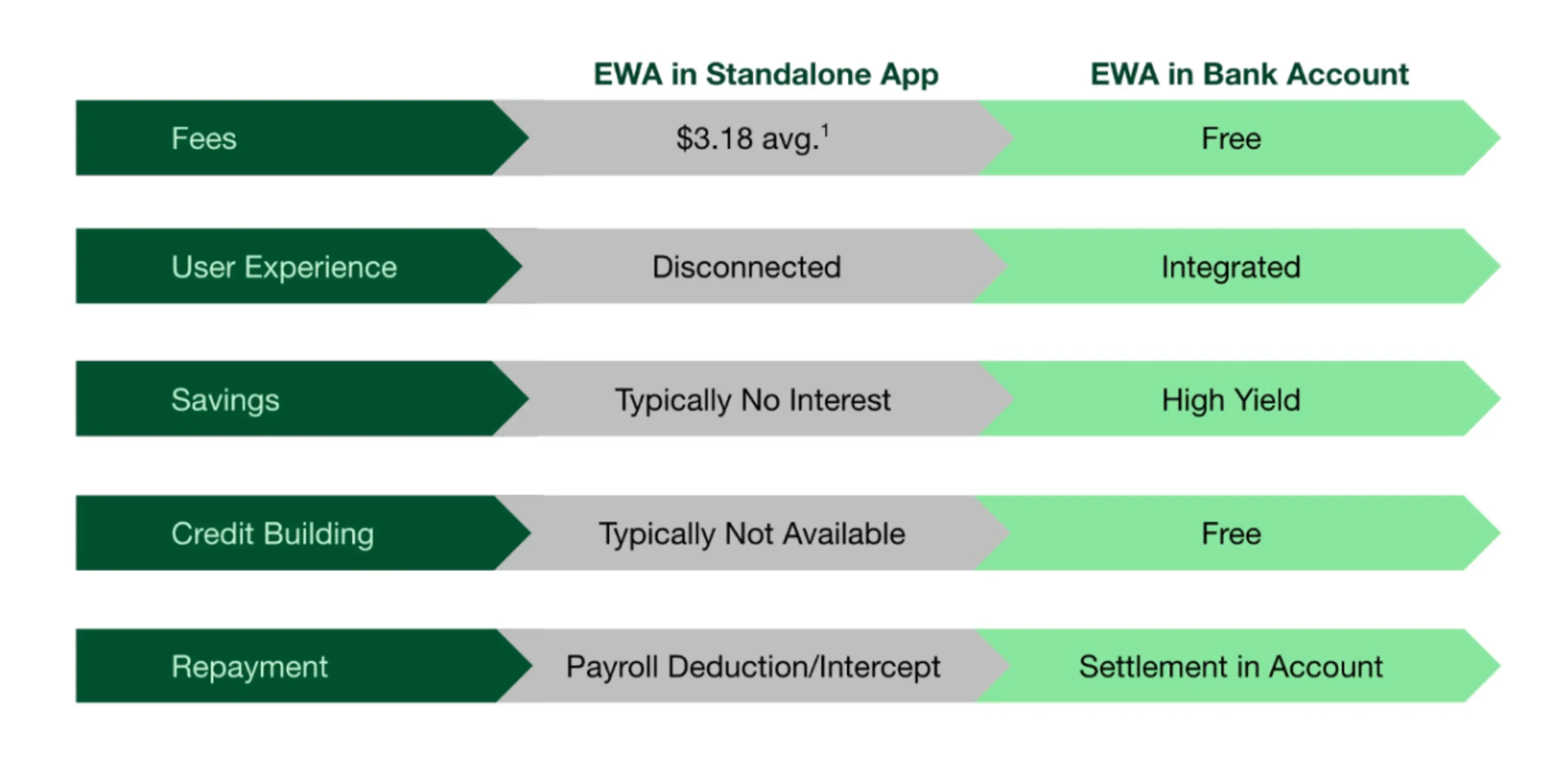

But EWA is most effective when it’s embedded in a bank account. And it can be fee-free thanks to the merchant-funded model where revenue comes from interchange, not user fees.

Without a banking relationship: instant access fees add up, funds are harder to manage, and financial tools are more limited.

1 CFPB (2024)

When EWA moves from a point solution to workplace banking, the experience changes materially. Funds move more efficiently. Employees have a command center to monitor, manage, save, and build from what they access. The benefit becomes more than a short-term solution — it becomes part of a longer-term financial pathway. And they save up to $3706 a year in transaction fees.

The same principle applies across the entire financial wellness stack.

Savings programs, credit-building tools, direct deposit, financial coaching — all of them perform better when banking is embedded.

This isn’t a collection of independent benefits. It’s a system. And banking is the infrastructure layer that makes the system work.

What HR Leaders Should Be Asking

The conversation among leading employers is shifting. A few years ago, the focus was adoption: Should we offer Earned Wage Access? Should we expand financial wellness benefits?

Now the focus is effectiveness: 8 out of 10 employers are struggling to capture financial wellness ROI.

The answer is often straightforward. The employees who need financial support the most are the least likely to have access to the system those benefits depend on. So the framing needs to change.

Instead of building from the top down — starting with retirement and working backward — employers can start with simpler questions:

Does every employee have access to a bank account?

Does our financial wellness benefit come embedded with everyday banking tools like EWA, Savings, credit building, and financial assistance?

If the answer is unclear, that’s a signal.

How Workplace Banking Can Scale

Workplace banking was initially local and relationship-driven. Employers partnered with nearby financial institutions — often credit unions — to offer employees access to basic banking services.

Those partnerships mattered. Credit unions, in particular, played an important role in expanding access to lower-cost financial services. They were community-based, member-owned, and often meaningfully improved financial outcomes for the workers they served.

But they were also built for a workforce that was:

Geographically concentrated

Long-tenured

Stable and predictable

Valued in-person retail experiences

That’s not what most employers operate today. Modern workforces are distributed, mobile, and increasingly composed of hourly, frontline, and gig workers. Turnover is higher. Geographic footprint is wider. Employment relationships are more fluid. And employees want everything to be instant.

A modern workplace banking benefit has emerged that:

Reaches every employee, regardless of location

Offers banking tools like no-fee checking and fee-free overdraft protection

Onboarding takes minutes, not days

Integrates directly with payroll

Connects seamlessly to EWA and other wellness tools like savings and credit building

Delivers a user experience strong enough that employees choose to use it

Has a plethora of tools for all employees at different stages of their financial journey

Provides an employer feedback loop: Tracks workforce savings rates, credit health and financial wellness ROI

The Bottom Line

Over the past decade, employers have built increasingly sophisticated financial wellness programs.

Those programs matter. They improve employee outcomes. They reduce stress. They support retention and productivity.

But they are only as effective as the foundation they’re built on.

Workplace banking is not an add-on. It is where financial wellness begins.

When every employee has access to a banking relationship:

EWA works better

Savings programs become actionable

Financial coaching becomes relevant

The entire system becomes more inclusive and more effective

The question isn’t whether workplace banking belongs in your strategy.

It’s whether your strategy can succeed without it.

Build the foundation first. Everything else compounds from there.

Learn about Chime WorkplaceTM

If you're ready to build a financial wellness program on a strong foundation, book a demo to see how Chime works for your workforce.

FAQs about Workplace Banking

Q: What is a workplace banking program?

A workplace banking program is a no-cost employer-sponsored benefit that connects employees with premium banking products and services, with enhanced features than would otherwise be available. Modern programs are typically mobile-first, meaning employees can open and manage accounts through an app without ever visiting a branch.

Q: How is workplace banking different from just having a bank account?

Traditional banking requires employees to find, open, and manage accounts entirely on their own. Workplace banking programs integrate directly into the employment relationship — activated at onboarding, connected to payroll, and often bundled with other financial wellness benefits like fee-free EWA, emergency savings, credit-building and financial coaching. Workplace banking is designed to have greater features and lower cost services than a standard consumer account. The employer channel makes banking easier to access, especially for employees who have historically been excluded from the financial system.

Q: Who benefits most from a workplace banking program?

All employees benefit from having a strong financial foundation, but workplace banking programs are especially impactful for unbanked and underbanked workers — including lower-income employees, hourly and frontline workers, recent immigrants, and others who face barriers to traditional banking. These are often the employees who are least served by standard financial wellness benefits and financial institutions.

Q: How many employees are actually unbanked or underbanked?

According to the FDIC1, 5.6 million U.S. households remain completely unbanked, and 19 million more are underbanked — meaning they have an account but still rely on costly alternatives like check cashers or payday lenders. Together, the unbanked and underbanked represent over 18% of the population. Among certain workforce segments, including lower-income workers and some minority communities, the rates are significantly higher than the national average. For most large employers, a meaningful portion of their workforce falls into this category.

Q: How does workplace banking connect to Earned Wage Access (EWA)?

EWA and workplace banking work best together. EWA gives employees faster access to wages they've already earned — a genuinely valuable benefit. But that access is most seamless and effective when employees have a bank account to receive and manage those funds. When banking and EWA are integrated, employees get a smoother experience, better financial flexibility, and more value from both benefits combined.

Q: Does offering workplace banking mean replacing our existing financial wellness benefits?

Not at all. Workplace banking is the foundation that makes everything else work better. Think of it as the infrastructure layer beneath your existing benefits stack. EWA, financial coaching, emergency savings, and credit-building tools all perform better — and reach more employees — when every worker has a banking relationship in place. It's additive, not a replacement.

Q: What should employers look for when evaluating a workplace banking provider?

Key criteria include: nationwide reach and accessibility regardless of where employees live, seamless payroll and direct deposit integration, mobile-first account opening with no credit history requirements, fee-free EWA, credit building, high-yield savings and other financial wellness tools, and a product experience compelling enough that employees actively choose to use it. The goal is a solution that works for every employee — not just those who already have financial stability.

Q: Where does workplace banking fit in our overall financial wellness strategy?

It's the starting point. Financial wellness programs are most effective when built from the bottom up — beginning with banking access, then layering in EWA, savings tools, coaching, and longer-term planning. Without that foundation, even the best-designed benefits will fail to reach the employees who need them most. Workplace banking isn't one item on the financial wellness menu — it's the table the whole menu sits on.

1 2023 FDIC National Survey of Unbanked and Underbanked Households

2 NBER, The Economics of Financial Stress

3 2024 EBRI Financial Wellbeing Employer Survey

4 TIAA Institute report finds ties between financial stress and mental health

5 Fintech Finance News, New Study Reveals Using Multiple Financial Apps is Necessity, Not Choice for Most Users

6 Based on Chime Workplace’s Strategic Financial Wellness partnership with Workday Wellness

Chime Workplace offered by Chime. Chime is a financial technology company, not a bank. Banking services provided by The Bancorp Bank, N.A. or Stride Bank, N.A., Members FDIC.

The Chime Visa® Debit Card is issued by The Bancorp Bank, N.A. or Stride Bank, N.A. pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa debit cards are accepted. The secured Chime Visa® Credit Card is issued by The Bancorp Bank, N.A. or Stride Bank, N.A. pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa credit cards are accepted. Please see the back of your Card for its issuing bank.

By clicking on some of the links above, you will leave the Chime website and be directed to a third-party website. The privacy practices of those third parties may differ from those of Chime. We recommend you review the privacy statements of those third party websites, as Chime is not responsible for those third parties' privacy or security practices.

Third-party trademarks referenced for informational purposes only; no endorsements implied.

Opinions, advice, services, or other information or content expressed or contributed here by customers, users, or others, are those of the respective author(s) or contributor(s) and do not necessarily state or reflect those of The Bancorp Bank, N.A. and Stride Bank N.A. ("Banks"). Banks are not responsible for the accuracy of any content provided by author(s) or contributor(s).

Address: 101 California Street, Floor 5, San Francisco, CA 94111, United States.

No customer support available at HQ. Customer support details available on the website.

© 2026 Chime Financial, Inc. All rights reserved.