Employer-integrated earned wage access (“EWA”) has moved from an experimental perk to a mainstream benefit for employers. Yet adoption at scale remains uneven - particularly among large, multi-state employers. According to new Everest Groups January 2026 report, The Reinvention of Earned Wage Access, 62% of employers cite regulatory concerns as the primary roadblock to adopting earned wage access.

That single data point suggests that many employers are evaluating models that address regulatory and compliance considerations.

Why EWA Fees Have Have Slowed Adoption

Earned wage access regulation in the U.S. remains fragmented. Recent CFPB commentary has addressed aspects of the federal regulatory landscape shifting attention to the states where differences around fee structures, wage assignment, licensing requirements, and repayment mechanics require careful consideration, especially for multi-state employers.

EWA fees are often the focus of regulatory scrutiny. Legacy EWA providers typically charge user fees because they have limited sources of revenue. The most common model is the instant access fee which averages $3.18 (according to Everest Group research.) These fees are often paired with a free option but they tend to be utilized infrequently because users prioritize immediate access.

Thirty-eight states have not yet enacted specific EWA laws or regulations, which may create uncertainty for employers as to what type of fees are permissible in each state. A prominent example is New York. In April 2025, the New York Attorney General sued a large EWA provider for violations, including fees that exceeded state usury limits. Legal actions like that can slow adoption, even when leadership believes the benefit itself is valuable.

For payroll, finance, and legal teams, the question is often “Should our workers be charged a fee for using an EWA benefit?” It’s not just an issue of compliance, but also of employee financial health.

Why EWA Wage Assignments Have Slowed Adoption

Fees aren’t the only regulatory risk surrounding EWA. How EWA providers get repaid is also an important consideration.

When EWA providers advance money to workers, they are generally repaid in one of three ways:

Deduction Model, where the employer deducts the amount of the advance already taken (plus any applicable fees) from the worker’s paycheck and sends the repayment directly to the EWA provider.

Payroll Intercept Model, in which the employer sends the entire paycheck to the EWA provider, who repays itself for the advance already taken (plus any applicable fees) before distributing the remaining pay to the employee.

Settlement Model, where the employer sends the entire paycheck to the worker’s bank account as usual, then settlement occurs from the bank account at the direction of the employee.

The Payroll Deduction and Payroll Intercept Models require a change to the payroll process. They also require the employer to redirect wage payments directly to the EWA provider. These payroll repayment models could create a risk that a state may deem the model akin to a wage assignment or improper wage deduction in that state. These laws often involve gray areas. For example, some states like California have wage assignment provisions in the labor code as well as the lending code. Some states have both wage deduction and wage assignment laws that could separately be implicated. These laws can impact both the employer and the EWA provider.

The Everest study found that 72% of surveyed employers indicated a preference for repayment to occur outside of payroll. The one model that may present fewer payroll process considerations is the Settlement Model, which requires no changes to payroll, no redirection of wages, and no additional compliance burden.

![[CE] Three Models of Earned Wage Access Repayment](/_ctf-img/ao7gxs2zk32d/64J3Vktmw4lVAdumLaFeqi/ced4feaea585c6b73af88228882e384d/ewa-payroll-compliance-models_EWA-B-1.png?fm=webp&w=800&fit=fill&q=50)

Why Legacy EWA Programs Can Remain Stuck in Evaluation Mode

The Everest Group finding reflects where the real decision-making friction occurs. Payroll, finance, and legal teams are responsible for ensuring wages are processed accurately and compliantly across jurisdictions. EWA is not evaluated as a standalone benefit. It is assessed as a payroll-adjacent program that intersects directly with wage laws, payment timing rules, and compliance obligations.

Many employers have delayed offering earned wage access until regulatory issues like fees and wage assignment are resolved. For multi-state organizations, the cost of getting compliance wrong can outweigh the upside of moving quickly.

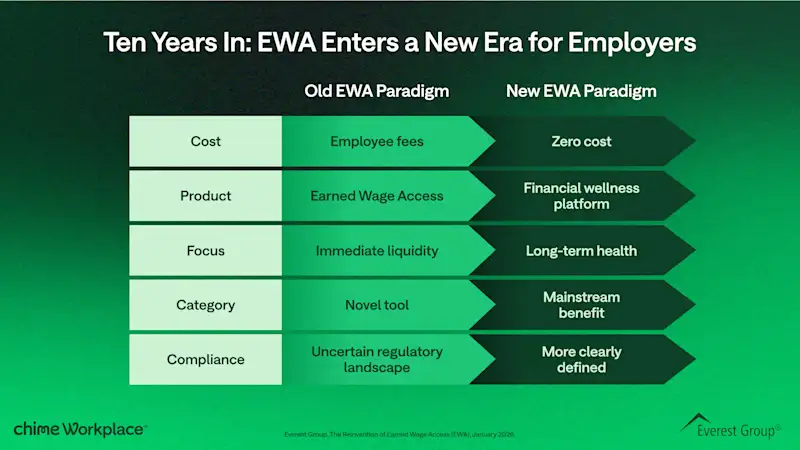

Legacy EWA programs that rely on fees or wage assignments may require additional evaluation by employers. The 62% figure reflects this reality. Regulatory considerations remain central to employer evaluation.

The New EWA Paradigm: Employer Sponsored model without fees and Designed with Compliance in mind

According to Everest Group, 56% of enterprises indicate a preference for zero-fee EWA models. And more than seven out of ten want the provider to handle repayment, meaning no more payroll deductions or wage assignment. They’ve been waiting for a better model.

The study identifies characteristics of emerging EWA models. The Everest study identifies a new EWA model that is designed to support broader financial wellness initiatives:

No-fee transactions

Financial wellness tools, beyond EWA

Integrates with payroll, without pay deductions

Designed to meet nationwide compliance standards

The Takeaway

Earned Wage Access adoption is influenced less by questions of value and more by employer considerations around payroll complexity according to 62% of respondents. The earned wage access model offered through Chime Workplace™, is structured with modern regulatory considerations in mind. Its employer sponsored settlement-based approach does not rely on employee transaction fees and is designed to operate across multiple jurisdictions, including states such as Maryland, New Jersey, California, New York. By facilitating payment outside of payroll redirection, the model is intended to reduce potential wage assignment and payroll deduction as regulatory frameworks continue to evolve.

Want to learn more about Chime Workplace? Let’s connect.