In 2025, the Consumer Financial Protection Bureau issued an advisory opinion clarifying how certain earned wage access (EWA) is not credit under the Truth in Lending Act and Regulation Z. The Bureau determined that employer-offered EWA settled through payroll processes is not considered credit under federal law when it meets specific structural criteria. This federal clarity helps employers better understand the regulatory treatment of EWA, while state wage, labor, and lending laws continue to apply.

Is EWA a loan?

Is earned wage access subject to state or federal lending laws? Over the last three years, several regulators and legislatures have begun to provide clarity at the state level:

California, Connecticut, and Maryland passed laws and regulations treating EWA as credit in their states.1 Together, these states represent 15% of the U.S. population.

Nine other states have passed laws specifically stating that EWA is not subject to state lending laws.2 Collectively, these states represent 12% of the U.S. population.

That leaves 38 states, representing 73% of the U.S. population, that have yet to pass laws or regulations addressing this question at the state level.

States That Currently Regulate Earned Wage Access

The CFPB issued an advisory opinion clarifying when EWA does not constitute credit under federal Truth in Lending rules—specifically when it is (i) free or (ii) employer-offered, aligned with payroll processes, limited to earned wages, and does not require employee repayment or create a debt obligation.

![[CE] Timeline Image- Earned wage access state & federal regulations timeline](/_ctf-img/ao7gxs2zk32d/64EXC9RYTgtGSbB88XC4kS/e6332b78cf8fc45ff76e4bd73c20494a/earned-wage-access-laws-per-state-timeline.png?fm=webp&w=800&fit=fill&q=50)

Industry leaders are responding to a rapidly changing landscape. While many EWA providers do not offer EWA structured as a loan under Regulation Z, this may be shifting.

Several states have recently enacted laws regulating EWA services, some regulating EWA as non credit, like Arkansas and Utah, while others regulate EWA under their existing lending frameworks, like Maryland and Connecticut. These developments show the ongoing evolution of state approaches to EWA beyond federal guidance.

What employers should consider now

Confirm whether your EWA model is employer-offered and integrated with the payroll process.

Understand how state wage deduction, assignment, and wage payment laws apply to your workforce.

Evaluate whether provider repayment methods introduce compliance risk in key states where you employ workers.

Align EWA with your broader financial wellness goals for your employees and communication strategy.

Source:

• https://mgaleg.maryland.gov/mgawebsite/Legislation/Details/hb1294?ys=2025rs

• https://portal.ct.gov/dol/knowledge-base/articles/wage-and-workplace-standards/wage-and-workplace-standards-division-notice-to-employers-utilizing-earned-wage-access-products?

• https://payroll.org/news-resources/news/news-detail/2025/04/03/arkansas-and-utah-latest-states-to-regulate-earned-wage-access-providers

![[CE] ewa-constructive-receipt-vs-loan_EWA-B-1](/_ctf-img/ao7gxs2zk32d/2dyA37pD2jTYSJOGJWL7Xy/1da3a4819e765f1cac518a84befc1117/ewa-constructive-receipt-vs-loan_EWA-B-1.png?fm=webp&w=800&fit=fill&q=50)

![[CE] Three Models of Earned Wage Access Repayment](/_ctf-img/ao7gxs2zk32d/64J3Vktmw4lVAdumLaFeqi/ced4feaea585c6b73af88228882e384d/ewa-payroll-compliance-models_EWA-B-1.png?fm=webp&w=800&fit=fill&q=50)

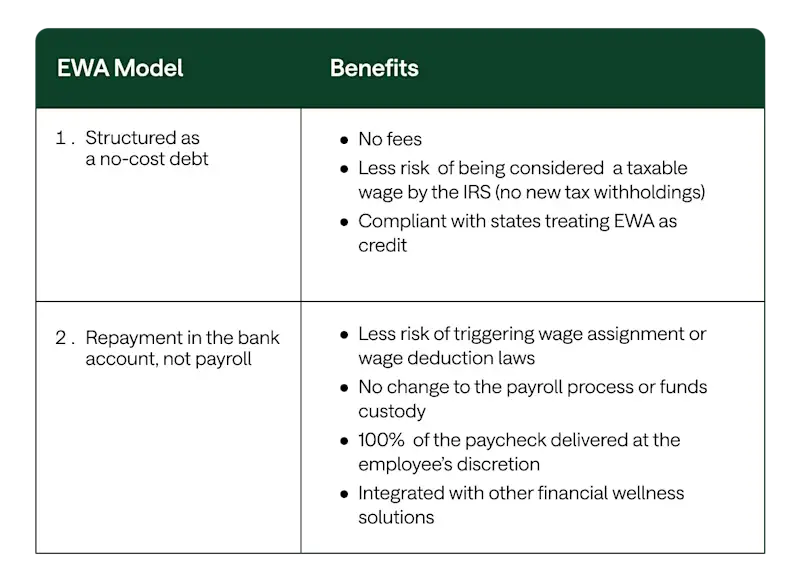

![[CE] Structured vs Not-Structured No-Cost Debt Table](/_ctf-img/ao7gxs2zk32d/2P7bLrdnnMkPO4NfPasul2/577cb6f7350a132a0bdddf3ac4843e39/Inline_Image_1220xFlex.png?fm=webp&w=800&fit=fill&q=50)